When homeowners stop paying mortgages, lenders may use foreclosure to recover owed money. In Ontario, Power of Sale is by far the most common remedy used by lenders, but the occasional foreclosure does happen. Power of Sale and foreclosure are two distinct legal processes with different outcomes. In Power of Sale, the lender sells the property to recover money, with any excess profits going to the homeowner.

In a foreclosure, the lender takes title to the property and all the equity in it. For this reason, it is recommended that the homeowner act immediately to try to stop the foreclosure. Typically, Power of Sale takes 6 months, while foreclosure takes at least a year to complete.

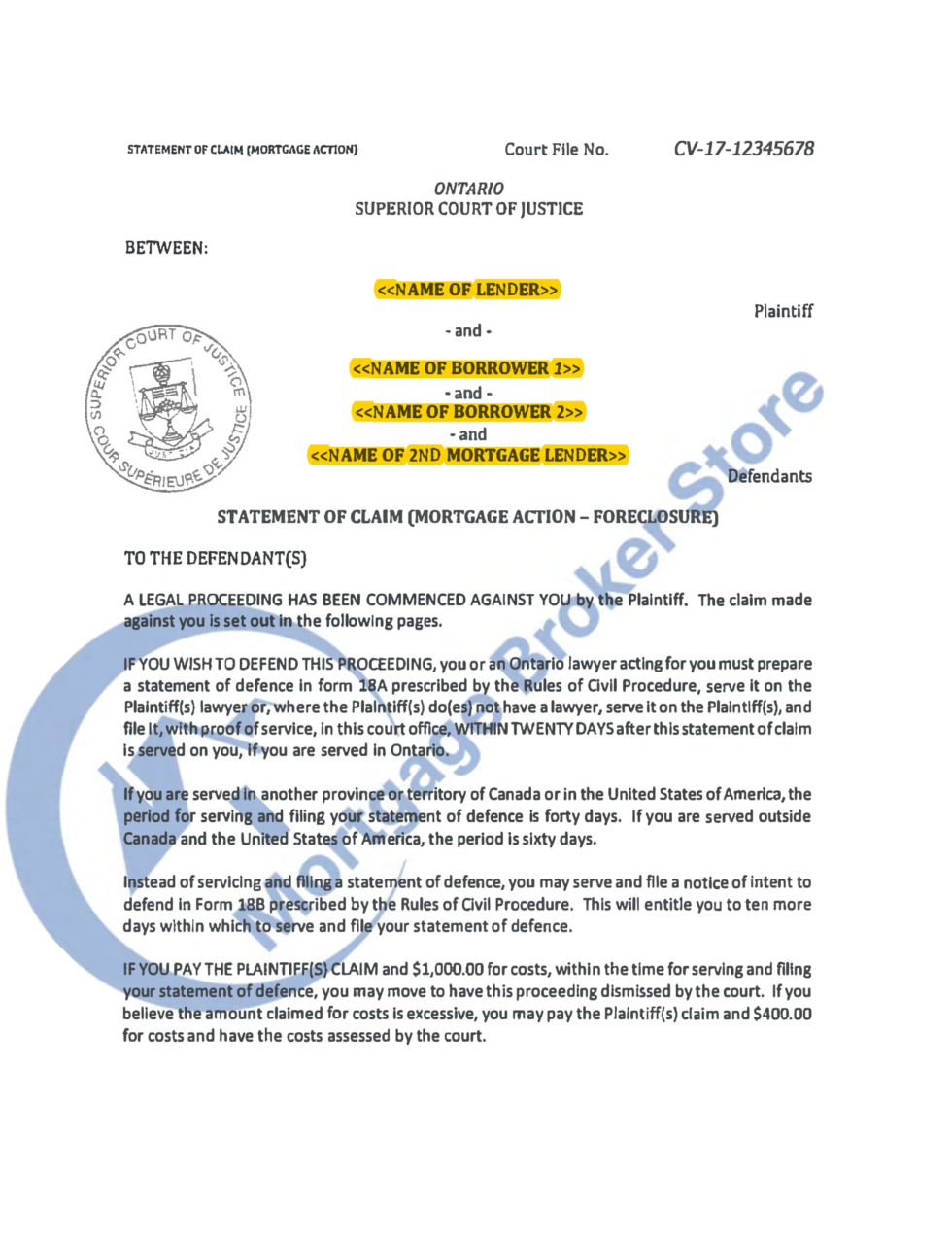

Both legal processes begin when a Notice of Sale is sent. The next document, the Statement of Claim will confirm the legal process being used; it will explicitly state that it is a “foreclosure action” near the top of the document.

What to Do If You Are in Foreclosure?

If you’ve received a Statement of Claim that states that you are in foreclosure, you have a few options available to you depending on when the document was sent and the amounts owing. The very first thing to try is to contact your lender and see if you can work out an arrangement to pay off what is owed. Some lenders will understand and work out a new payment plan or new financing to bring the mortgage back into good standing. However, in many cases, the lender will not be willing to negotiate and will demand payment.

The Statement of Claim document specifies the amount demanded by the lender and the deadline for payment. This amount is typically the value of the arrears plus fees. After the last day to pay has passed, the full amount of the mortgage plus fees will be due. In an Ontario foreclosure, the homeowner can also make a request for sale to convert the foreclosure process into a Power of Sale process. Filing a request for sale is recommended if the value of the property far exceeds the value of the mortgage. If you are unable to negotiate with the lender, you can still arrange new financing to pay them off or sell the property.

Want to learn more about Power of Sale?

Contact us for a free consultation

Getting New Financing to Stop the Foreclosure

In many cases, the lender will refuse to make any extra arrangements and will simply want what they are owed. Since someone in foreclosure is considered to be a high-risk client, most banks and large lending institutions will turn them down. There are many private lenders that can offer mortgages to people in Power of Sale or foreclosure, but it requires that the property has sufficient equity. Most private lenders can approve a mortgage as long as the total value of the mortgage on the property is not in excess of 80% of its estimated value.

If the first mortgage lender is asking for arrears plus fees, then a private lender can provide a new second mortgage to pay the first mortgage lender. And, if the second mortgage lender is threatening foreclosure, then the private lender can replace the existing second mortgage with a new one. If the first mortgage holder is requesting the entire mortgage, then a private lender may be able to buy out that mortgage to stop the foreclosure. Many of these private lenders do not advertise, making it advisable to contact a mortgage broker for assistance.

Selling the Property to Stop the Foreclosure

Stopping a Home Foreclosure

If an Ontario homeowner has fallen into arrears with the monthly mortgage payments there will be two legal processes that a lender will choose from to try to bring the property into good standing, or take possession of the property to sell it.

Overwhelmingly, in Ontario, the legal process that most lenders choose to use when dealing with mortgage default is the Power of Sale. However, some Ontario-based lenders do, on occasion, initiate the process of foreclosure in an attempt to not only sell the property that is in arrears but also take over the title on the property.

Foreclosure is a fairly lengthy legal process used for dealing with mortgage defaults. It can take up to a year to finalize and involve the courts. It usually takes up to 6 missed mortgage payments for your lender to send the first letter, referred to as a notice of sale initiating foreclosure proceedings. Keeping the courts out of the default process is preferred by Ontario-based lenders. If you’ve received a statement of claim for foreclosure, it’s crucial to act to prevent costs and potential title loss.

Ways to Stop Foreclosure of Your Property

An Ontario homeowner has time to stop the foreclosure process by bringing the mortgage into good standing. Several options are available:

1. Obtain a private loan to bring the mortgage in good standing– Private loan options are available for high-risk situations where banks won’t lend. You can apply for a second mortgage or home equity loan to settle mortgage arrears. Private lenders offer loans up to 75% of your home’s value at rates from 7% to 10%, based on your home equity.

2. Refinance the first mortgage– Look at the option of refinancing the first mortgage through a private lender allowing for arrears to be paid and manageable monthly mortgage payments moving forward.

3. Try to negotiate with the lender- There is always the option of trying to work out a payment arrangement with your lender and trying to change some of the terms of the mortgage loan enabling you to catch up with any arrears owing on the property.

4. Have a private lender buy out the mortgage– Some private lenders might consider buying out your current mortgage if the equity warrants such a decision.

5. Ask for a request for sale to change foreclosure to the Power of Sale- Ontario homeowners can request to change from foreclosure to Power of Sale to sell with retained title and equity.

6. Sell house “as is” to a buyer for cash- There are buyers in Ontario who will buy your house for cash at a discount in the state it is currently in. This would enable you to avoid the costly foreclosure process and there is no need to put money into renovations or fix-ups before the sale of the property.

Let Mortgage Broker Store Help You

Ontario homeowners should take every step possible to prevent foreclosure on their home. There are options available. At Mortgage Broker Store we will be able to inform you of all options open to your specific set of financial circumstances.

We will steer you towards private lenders who will be able to offer secured private mortgage loan options.

Short-term private mortgage loans can bring your mortgage up to date and prevent foreclosure on your house. Call 647-931-5396 or email jonathan@powerofsalesontario.ca and gain expert advice!

Stop Power of Sale and Foreclosure in Cities and Towns Across Ontario, Including:

- Stop Ajax Power of Sale and Foreclosure

- Stop Aurora Power of Sale and Foreclosure

- Stop Barrie Power of Sale and Foreclosure

- Stop Belleville Power of Sale and Foreclosure

- Stop Bradford Power of Sale and Foreclosure

- Stop Brampton Power of Sale and Foreclosure

- Stop Brant Power of Sale and Foreclosure

- Stop Brantford Power of Sale and Foreclosure

- Stop Burlington Power of Sale and Foreclosure

- Stop Caledon Power of Sale and Foreclosure

- Stop Cambridge Power of Sale and Foreclosure

- Stop Cornwall Power of Sale and Foreclosure

- Stop Fort Erie Power of Sale and Foreclosure

- Stop Georgina Power of Sale and Foreclosure

- Stop Guelph Power of Sale and Foreclosure

- Stop Halton Hills Power of Sale and Foreclosure

- Stop Hamilton Power of Sale and Foreclosure

- Stop Innisfil Power of Sale and Foreclosure

- Stop Kingston Power of Sale and Foreclosure

- Stop Kitchener Power of Sale and Foreclosure

- Stop London Power of Sale and Foreclosure

- Stop Markham Power of Sale and Foreclosure

- Stop Milton Power of Sale and Foreclosure

- Stop Mississauga Power of Sale and Foreclosure

- Stop Newmarket Power of Sale and Foreclosure

- Stop Niagara Falls Power of Sale and Foreclosure

- Stop North Bay Power of Sale and Foreclosure

- Stop Oakville Power of Sale and Foreclosure

- Stop Orangeville Power of Sale and Foreclosure

- Stop Orillia Power of Sale and Foreclosure

- Stop Oshawa Power of Sale and Foreclosure

- Stop Ottawa Power of Sale and Foreclosure

- Stop Peterborough Power of Sale and Foreclosure

- Stop Pickering Power of Sale and Foreclosure

- Stop Richmond Hill Power of Sale and Foreclosure

- Stop Sarnia Power of Sale and Foreclosure

- Stop Sault Ste. Marie Power of Sale and Foreclosure

- Stop St. Catharines Power of Sale and Foreclosure

- Stop St. Thomas Power of Sale and Foreclosure

- Stop Stouffville Power of Sale and Foreclosure

- Stop Stratford Power of Sale and Foreclosure

- Stop Sudbury Power of Sale and Foreclosure

- Stop Thunder Bay Power of Sale and Foreclosure

- Stop Timmins Power of Sale and Foreclosure

- Stop Toronto Power of Sale and Foreclosure

- Stop Vaughan Power of Sale and Foreclosure

- Stop Waterloo Power of Sale and Foreclosure

- Stop Welland Power of Sale and Foreclosure

- Stop Whitby Power of Sale and Foreclosure

- Stop Windsor Power of Sale and Foreclosure

- Stop Woodstock Power of Sale and Foreclosure