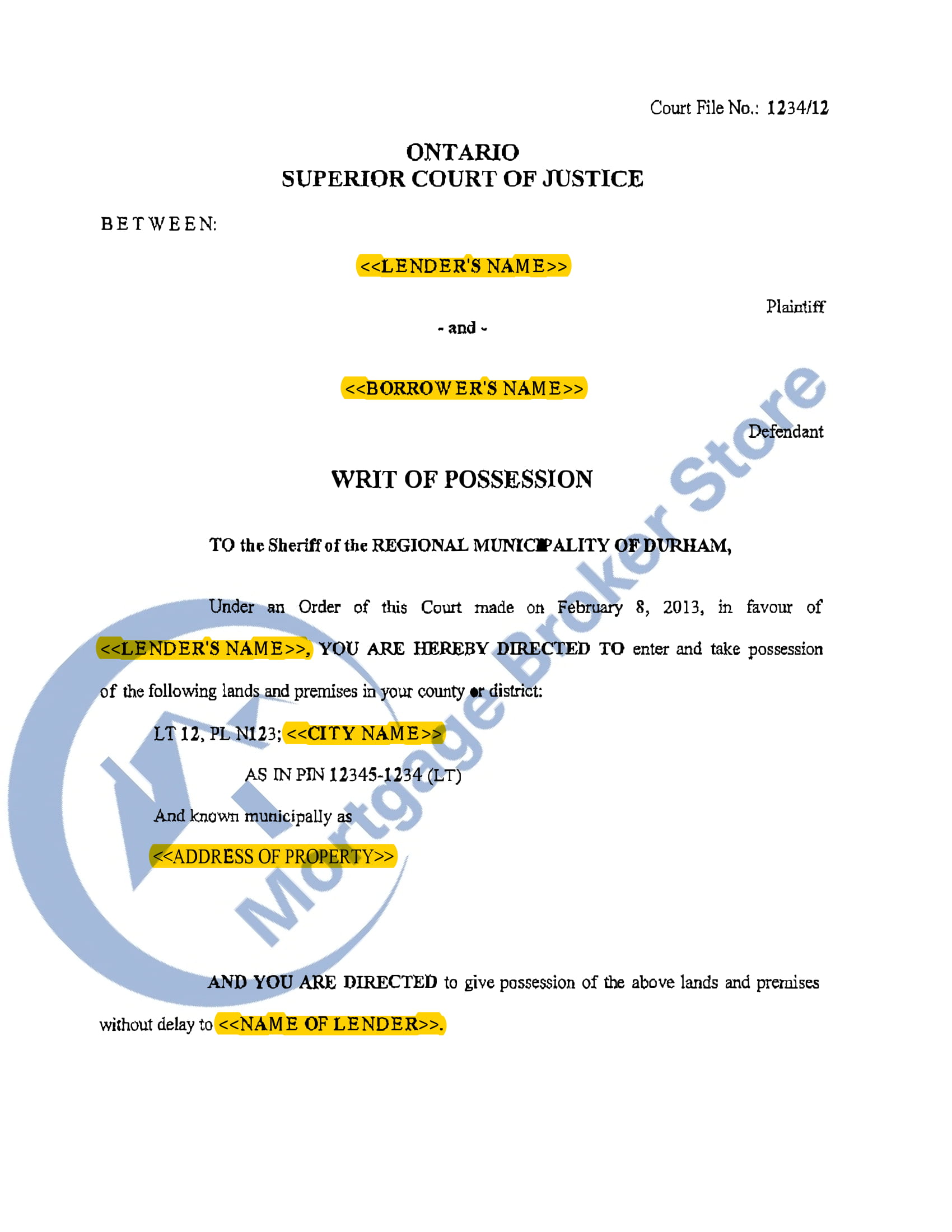

Writ of Possession is one of the many documents involved in the Power of Sale process. The Writ of Possession is issued by the courts after the lender has obtained judgment on their Statement of Claim. The Writ of Possession is sent to all involved parties, including lenders, occupants, owners, and the sheriff’s office. Once the sheriff’s office receives the Writ, they schedule eviction of occupants, handing property control to the lender. The document, titled ‘Writ of Possession,’ clearly grants the lender authority to take possession of the property.

What Happens After a Writ of Possession

After the Writ of Possession is issued, the sheriff’s office begins to process the eviction paperwork. The sheriff will typically give 2 weeks’ notice of the eviction and send an Eviction Notice to the property. After sending the Writ of Possession, occupants are typically evicted within about 30 days on average. Once the lender has possession of the property, they will arrange to sell it, typically with a licensed real estate agent. Once the property is sold, any excess profit is given to the homeowner. However, legal and administrative fees for processing the Power of Sale are deducted from the sales proceeds, which, in many cases, eats up all the money which would have gone to the homeowner.

Methods for Fixing the Situation

If you are looking to stop a Power of Sale after a Writ of Possession has been sent, you must act quickly since there will not be a lot of time left. In the majority of cases, the lenders will refuse to accept any payment aside from the full amount of the mortgage plus fees. One method of stopping the Power of Sale is to apply for a new mortgage to replace the problematic mortgage. Alternatively, if you sell the property before the eviction, then all legal actions will be stopped. Some people choose to get a new mortgage and sell the property over the course of several months, which would allow for renovations and more comprehensive marketing of the property.

If a mortgage lender does not receive payment from a borrower, they’ll be forced to act or risk losing their investment. The most common method of recovering an investment is to sell a property via Power of Sale. The third step in the Power of Sale process is the Writ of Possession, which comes after the Notice of Sale and Statement of Claim documents. The Writ of Possession is, simply put, a request to a superior court judge1 to allow the lender to evict and take possession of a property. Once the judge has reviewed the Writ of Possession, they can grant Judgment for Possession, which allows the lender to file an eviction request with the local sheriff’s office2.

Reasons For Power For Power of Sale

There are many reasons why a mortgage lender would have to resort to Power of Sale:

- The homeowner fails to keep the property insured

- Failure to pay mortgage payments

- Unauthorized damage to or use of the property

- Failing to follow any other terms of the mortgage contract

There are many steps involved in a Power of Sale action, but once the homeowner loses access to their property, they are more limited in their ability to revolve the situation. Once the Writ of Possession is issued by the mortgage lender, the final steps of the Power of Sale process are set in motion.

Writ of Possession in Ontario remains in force for one year from the date of the order. It can then be renewed for one year from each renewal.

Occupants are given a date they are required to move out, after which an eviction notice can be issued.

Upon getting a Writ of Possession from a mortgage lender, start to prepare for the next steps:

- Do the current occupants of the property understand the situation?

- Are all the occupants able to find alternative living arrangements?

- Can you move out the property’s contents before the eviction?

- Is it possible to sell the property before the eviction day?

- Have you already consulted with other mortgage brokers and lenders about getting a new mortgage?

If you are the owner of the property, you still may be able to prevent the lender from taking possession. Always keep copies of all receipts and documents to ensure there are no legal questions in the event the lender wants to adjust the arrangement.

Important Legal Notice

This article is meant as a general informational resource, and you should also consult a professional when dealing with a Writ of Possession and a Power of Sale. There are many variables and potential conflicts involved in fixing a Power of Sale situation. Our team deals with these situations on a daily basis and can give free advice upon request. To get in touch with us, please call 416-499-2122 or email jonathan@powerofsalesontario.ca.

Although it is always preferable to try to ensure that any mortgage payments that you may have are in good standing and do not fall into arrears, sometimes finances become too tight to make your mortgage payments reliably. Your lender may take legal action to try to sell your property if your mortgage goes into default. Depending on your lender, there are two legal routes to address mortgage default3 and attempt property sale.

In Ontario, lenders overwhelmingly tend to use the Power of Sale to try to recoup losses but there are some mortgage arrangements where a lender may choose foreclosure as the method to deal with mortgage default.

Depending on the method used to address mortgage default, your lender must follow legal steps before forcing you to vacate and sell the property. There is time to try to put your mortgage in good standing before either process is initiated by your lender.

In a Power of Sale, your lender must give you 15 days before notifying you of impending actions. In foreclosure, lenders typically wait for up to six missed mortgage payments before sending a Notice of Sale letter.

What Is a Writ of Execution?

An Ontario homeowner in mortgage arrears cannot be evicted or have their property sold until due process is completed. One of the last steps in Power of Sale and foreclosure is obtaining the Writ of Execution and Writ of Possession. In Ontario’s Power of Sale, a Writ of Possession is needed to sell the property legally, owned by the homeowner. There is no change in the title.

In the foreclosure process, the title is reverting to the lender. To sell the property legally, obtain a Writ of Execution for lender possession, sale, and title transfer.

A Writ of Execution is a court order sent to a sheriff to enforce a judgment made by the courts. The Writ of Execution is a final step in foreclosure, allowing your lender to legally possess and sell your property.

A lender must obtain a Writ of Execution to legally sell a property and issue an eviction notice for homeowner removal. Neither lenders nor Ontario real estate lawyers can physically evict homeowners from their property. This duty is performed by a sheriff after he/she has been sent the Writ of Execution from the court.

Notice of Sale vs. Statement of Claim vs. Writ of Possession

These three documents mark the escalating stages of the Ontario power of sale process. The earlier the document you have received, the more options you still have.

| Aspect | Step 1 · Early Warning Notice of Sale | Step 2 · Court Action Statement of Claim | Step 3 · Final Enforcement Writ of Possession |

|---|---|---|---|

| What it is | A legal notice from your lender warning that the power of sale process has started. | A court document claiming the mortgage debt and possession of the property. | A court order that lets the sheriff remove occupants and hand the property to the lender. |

| Who issues it | The lender, usually through a lawyer, sent by registered mail. | The lender’s lawyer, issued through the Ontario Superior Court of Justice. | The court, after the lender obtains judgment on its Statement of Claim. |

| When it arrives | At least 15 days after your mortgage goes into default — the first step of the process. | After the Notice of Sale period passes without payment. | After judgment — the sheriff schedules the eviction once the writ is received. |

| Your time to respond | About 30 days to bring the mortgage back into good standing. | About 30 days to pay the claim, or 20 days to file a Statement of Defence. | Very little time — the sheriff usually acts within a week or two. |

| What you can still do | Most options are still open: pay the arrears, refinance, negotiate with the lender, or sell on your own terms. | Options are narrowing: pay the claim, refinance quickly, or file a defence — acting fast matters. | Urgent: only immediate payment, refinancing, or emergency legal action can stop the eviction. |

Let Us Help Keep Possession of Your Home

Our team has expert knowledge about the Power of Sale and foreclosure process. We are here to help you explore your options to stop losing possession of your home. If facing Power of Sale or foreclosure, we connect you with private lenders for mortgage solutions to retain your home. Call 416-499-2122 or email jonathan@powerofsalesontario.ca and gain expert advice!

References

- Rules of Civil Procedure, R.R.O. 1990, Reg. 194, Rule 60.10 — a writ of possession may be issued only with leave of the court ↩︎

- Rules of Civil Procedure, R.R.O. 1990, Reg. 194, Rule 60.03 — an order for possession of land may be enforced through a writ of possession ↩︎

- Rules of Civil Procedure, R.R.O. 1990, Reg. 194, Rule 64 — mortgage actions and possession claims ↩︎

Disclaimer: This page is for general informational purposes only and should not be taken as legal, financial, mortgage, or real estate advice. Power of sale and foreclosure matters can have serious consequences, and you should speak with a licensed mortgage professional, lawyer, or qualified advisor before making decisions. Power of Sales Ontario does not guarantee results, mortgage approval, or that the information on this page applies to your specific situation.