A Notice of Sale (formally a Notice of Sale Under Mortgage) is the first document a lender serves to start Ontario’s power of sale process. It can be issued once a mortgage default has lasted at least 15 days, and it opens a 35-to-40-day window to bring the mortgage back into good standing before the lender can act further.

A Notice of Sale is a legal document a lender sends to a borrower defaulting on their mortgage. A Notice of Sale can be sent at least 15 days after the default and is the first step in the Power of Sale process. This document is sent to all mortgage holders, lenders, and anyone with an interest in the property. Typically, a lawyer sub-searches the title and sends the Notice of Sale via registered mail.

Under section 32 of Ontario’s Mortgages Act1, a Notice of Sale Under Mortgage generally cannot be given until the mortgage default has continued for at least 15 days. Recipients of this notice include the property owner, spouses, tenants, mortgage holders, lien claimants, and guarantors. Section 33 of the Mortgages Act2 sets out how the notice must be served and who is entitled to receive it.

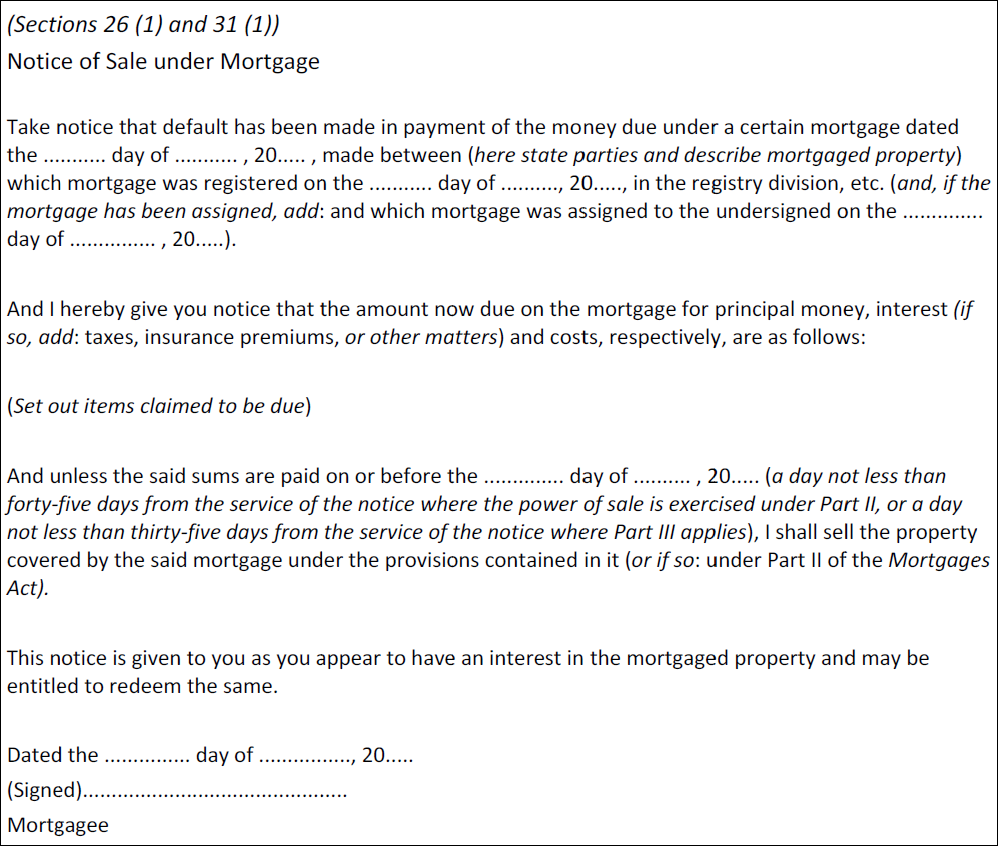

This document is identified by the title “Notice of Sale under Mortgage” at the top. Section 31 of the Mortgages Act3 defines the notice’s contents, stating the default, required payments, and payment deadlines, and the official document is prescribed as Form 1 under O. Reg. 814/214. Below is the sample document from the Ontario government.

What a Notice of Sale Must Contain (Mortgages Act Requirements)

A valid Notice of Sale is not a free-form letter. Section 31 of the Mortgages Act and the prescribed Form 1 under O. Reg. 814/21 require it to set out:

- The mortgage and property in default — the date of the mortgage, the parties to it, and the property it covers, so you know exactly which loan is being enforced.

- The amounts owing, itemized — principal, interest, arrears, taxes, insurance premiums and enforcement costs are listed separately, so you can see exactly what the lender claims.

- The payment deadline (redemption date) — the date by which you can pay the amounts claimed and stop the sale: at least 35 days from when the notice is served, or 40 days where a spouse occupies the home.

- A warning of what happens next — that the property will be sold under the power of sale in the mortgage if payment is not made by the deadline.

- Service on everyone with an interest — under section 33, the owner, spouses, tenants, later mortgage holders, lien claimants and guarantors must all receive the notice, typically by registered mail.

To see how these requirements look on a real document, review our Notice of Sale example 1 and example 2, or see real Notice of Sale examples alongside the other documents used during a power of sale. If the amounts, dates or list of people served look wrong, raise it when you get advice — errors can affect the lender’s ability to proceed.

What Happens After?

After sending the Notice of Sale, the lender must wait 35 days, or 40 if a married couple occupies the property, before proceeding with the Power of Sale. The longer 40-day period reflects the matrimonial home protections under sections 21 and 22 of the Family Law Act5, which can apply when a spouse occupies the property. These 35 to 40 days are known as the redemption period, and under section 42 of the Mortgages Act6 the lender cannot take further steps to enforce the mortgage during this waiting period. The lender must accept payment of the items listed in the Notice of Sale during this time period. Under section 43 of the Mortgages Act, once paid, the mortgage returns to good standing and operations resume normally. If the mortgage goes unpaid, the lender may file for a Writ of Possession, enabling them to evict homeowners. After the redemption period, the lender can demand payment of the entire mortgage, not just the Notice of Sale amount. An average Power of Sale in Ontario takes around 3 months to be complete from beginning to end.

The redemption period is not just a waiting period — it is your window to act. Paying the amounts listed in the notice restores the mortgage, and most lenders would rather be paid than sell. For a step-by-step look at what happens during these 35 to 40 days, read how the redemption period works in Ontario’s power of sale process.

Notice of Sale vs. Statement of Claim vs. Writ of Possession

These three documents mark the escalating stages of the Ontario power of sale process. The earlier the document you have received, the more options you still have.

| Aspect | Step 1 · Early Warning Notice of Sale | Step 2 · Court Action Statement of Claim | Step 3 · Final Enforcement Writ of Possession |

|---|---|---|---|

| What it is | A legal notice from your lender warning that the power of sale process has started. | A court document claiming the mortgage debt and possession of the property. | A court order that lets the sheriff remove occupants and hand the property to the lender. |

| Who issues it | The lender, usually through a lawyer, sent by registered mail. | The lender’s lawyer, issued through the Ontario Superior Court of Justice. | The court, after the lender obtains judgment on its Statement of Claim. |

| When it arrives | At least 15 days after your mortgage goes into default — the first step of the process. | After the Notice of Sale period passes without payment. | After judgment — the sheriff schedules the eviction once the writ is received. |

| Your time to respond | About 30 days to bring the mortgage back into good standing. | About 30 days to pay the claim, or 20 days to file a Statement of Defence. | Very little time — the sheriff usually acts within a week or two. |

| What you can still do | Most options are still open: pay the arrears, refinance, negotiate with the lender, or sell on your own terms. | Options are narrowing: pay the claim, refinance quickly, or file a defence — acting fast matters. | Urgent: only immediate payment, refinancing, or emergency legal action can stop the eviction. |

How to Remedy the Situation

Once you receive a Notice of Sale, it is important to act quickly to resolve the issue.

During Power of Sale, the lender charges legal and administrative fees to the mortgage, reducing the homeowner’s equity.

Contact the mortgage lender immediately upon receiving it. The lender may be able to arrange for you to bring the mortgage back into good standing. In most cases, bringing the mortgage back into good standing means the borrower must get new financing, they must refinance an existing mortgage, or, if financing isn’t possible arrange to sell the property.

Important Legal Notice

This page provides general information; it doesn’t cover every detail of a Notice of Sale. It is important for a borrower under Power of Sale to contact a professional to discuss their options. The team at powerofsalesontario.ca faces these kinds of scenarios on a daily basis, and is available for a free consultation by calling 416-499-2122 or emailing jonathan@powerofsalesontario.ca

References

- Mortgages Act, R.S.O. 1990, c. M.40, s. 32 — timing of the notice and waiting period ↩︎

- Mortgages Act, R.S.O. 1990, c. M.40, s. 33 — service and recipients of the notice ↩︎

- Mortgages Act, R.S.O. 1990, c. M.40, s. 31 — form and contents of the Notice of Sale ↩︎

- O. Reg. 814/21: Forms — prescribed Form 1, Notice of Sale Under Mortgage ↩︎

- Family Law Act, R.S.O. 1990, c. F.3, ss. 21–22 — matrimonial home issues where applicable ↩︎

- Mortgages Act, R.S.O. 1990, c. M.40, ss. 42–43 — proceedings during the notice period and payment/redemption rights ↩︎

Disclaimer: This page is for general informational purposes only and should not be taken as legal, financial, mortgage, or real estate advice. Power of sale and foreclosure matters can have serious consequences, and you should speak with a licensed mortgage professional, lawyer, or qualified advisor before making decisions. Power of Sales Ontario does not guarantee results, mortgage approval, or that the information on this page applies to your specific situation.