Yes, a power of sale in Ontario can often be stopped before the property is sold. Depending on your situation, this may involve paying the arrears, refinancing, arranging a private mortgage, selling the property voluntarily, or negotiating with the lender. The sooner you act, the more options you may have.

Do you need help to avoid or stop a Power of Sale or Foreclosure? Have you missed mortgage payments, and your lender has threatened to start legal action against your property? Do you want to prevent an eviction? If you are in any of these situations, read on to learn about the best way to resolve your situation.

Our company has over a decade of experience in working with homeowners in Power of Sale and foreclosure situations. While this advice will be applicable to most homeowners, Power of Sale and foreclosure can be a complex and lengthy process. It is always good to get a second opinion, and our company offers free consultations to those who call at 416-499-2122.

What Does Power of Sale Mean in Ontario?

Power of Sale is the most commonly used method for mortgage lenders to recover their investment. This method was created as an alternative to the foreclosure process, which is far more resource-intensive and time-consuming. A Power of Sale action can be started by a mortgage lender when the borrower has broken the terms of the mortgage agreement or has failed to renew the mortgage. Most commonly, this means that the borrower has missed their monthly payments, but it can also happen due to failure to uphold other terms of the mortgage. Other common breaches of mortgage terms include failure to insure the property, causing substantial damage to the property, or failure to pay property taxes.

Whatever the situation, it is important to note that the homeowner has full rights to the property up until the day of eviction. The homeowner is free to remortgage or sell the property while the Power of Sale process is ongoing. Once the property is sold, the former homeowner then loses all rights to the property.

Power of Sale vs. Foreclosure in Ontario

Mortgage lenders in Ontario have two legal options when a borrower defaults, Power of Sale or Foreclosure. In a Power of Sale, the lender sells the property on the open market to pay off all debts. Once the property is sold, any excess profits must be given to the homeowner. This is very different from the Foreclosure process, which gives the lender title to the property and leaves nothing for the homeowner.

In Ontario, Power of Sale is the most commonly used legal process since it is generally faster and incurs fewer fees than foreclosure. If the Statement of Claim for your mortgage action1 says “Foreclosure,” then your property is in Foreclosure. If you do not see the word “Foreclosure,” then this claim will be a Power of Sale.

The Ontario Power of Sale Timeline

Since resolving a Power of Sale can be a very time-sensitive matter, it is important to understand how far along you are in the process. The entire process for a typical Power of Sale in Ontario takes 4 to 6 months to complete. Some methods of resolution can take weeks or months and may not work if you are close to eviction.

Every lender is required to follow certain legal steps in the Power of Sale process as outlined below.

- Notice of Sale

- Statement of Claim

- Notice of Possession

- Writ of Possession

- Sheriff Sends Notice to Vacate to the Borrower

Step 1: Mortgage Default

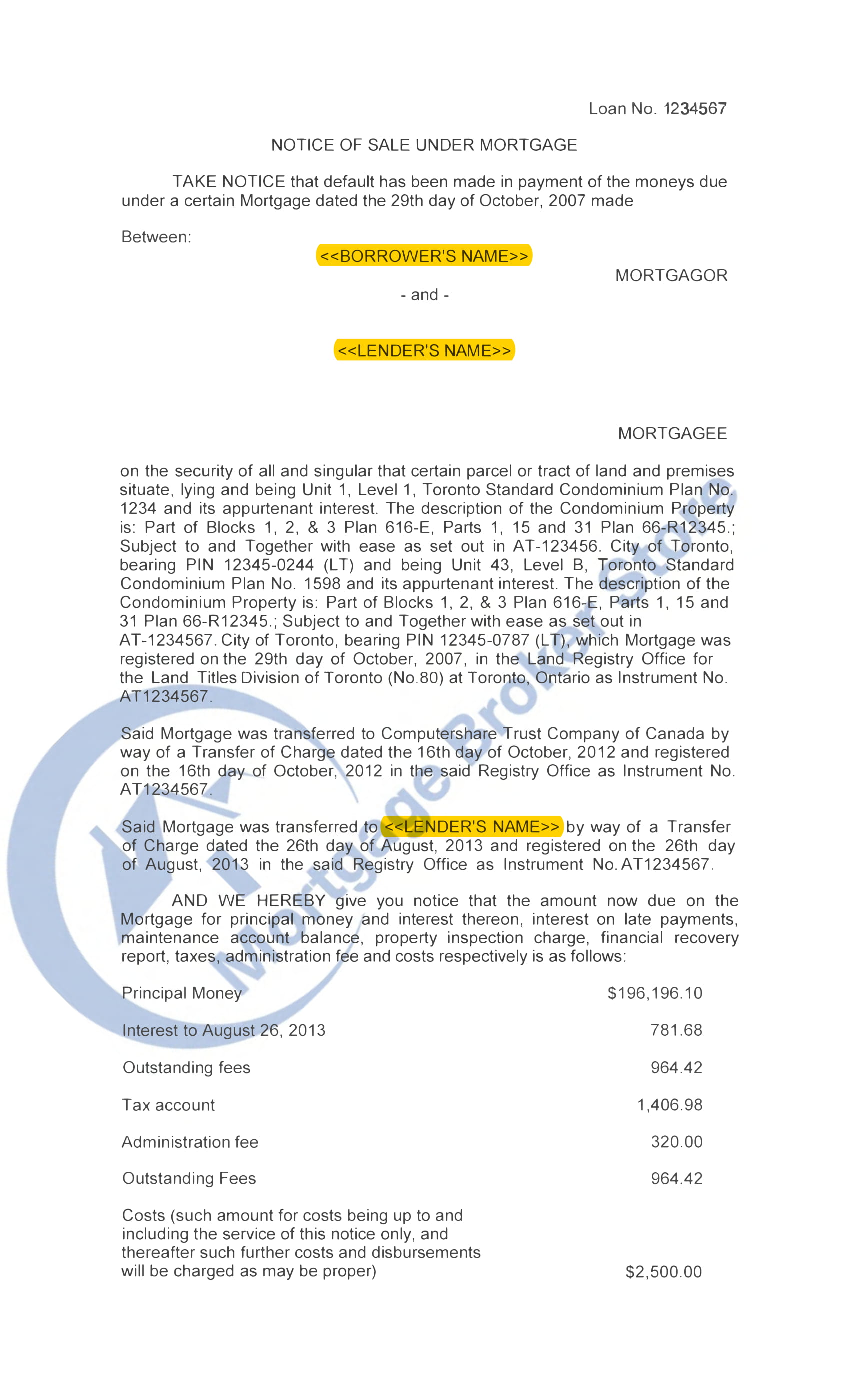

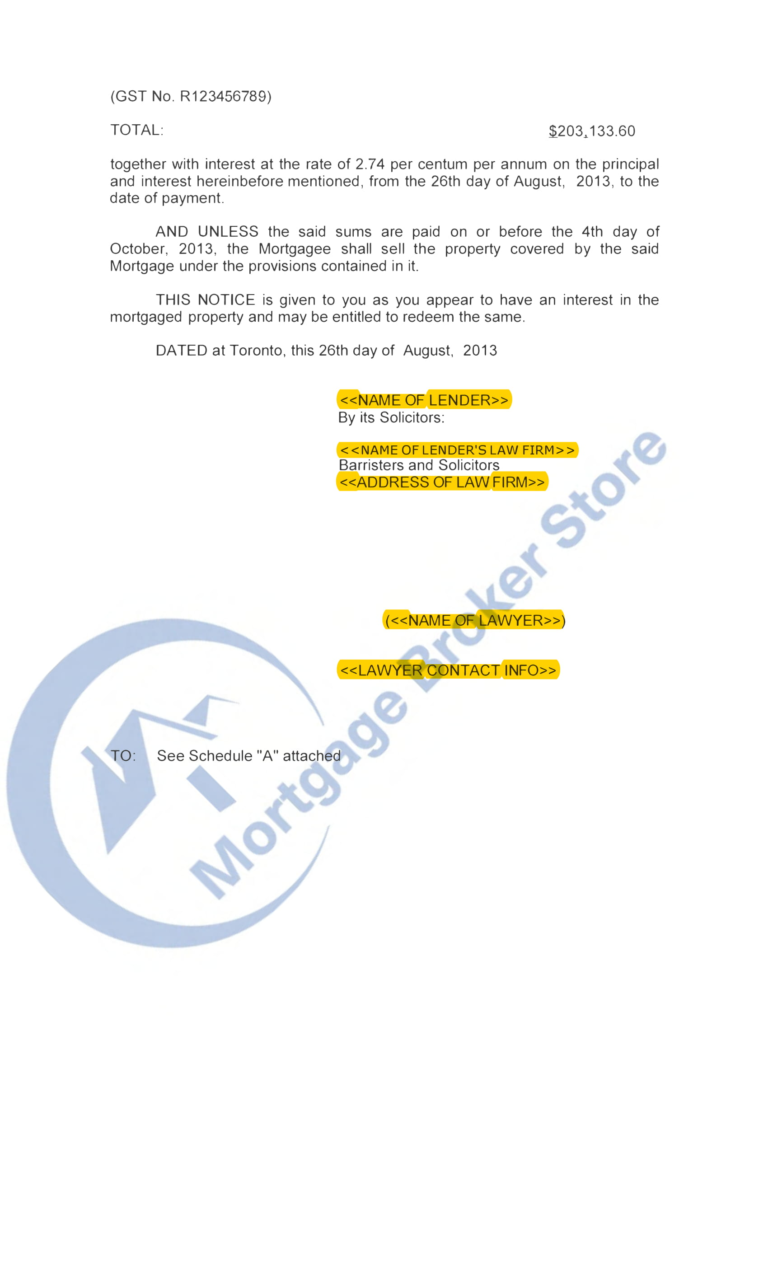

Before a lender can start the Power of Sale process, the borrower must be in breach of one or more of the mortgage terms. The lender must notify the borrower of the mortgage default. Most lenders will call or mail homeowners a “Default Notice” or “Demand Letter” to notify the borrowers. The Notice of Sale marks the official start of the legal process and should state the amount owed and the cause of default. It will also have the contact information of the lender or their legal representative. Once the Power of Sale has begun, most lenders will insist that the borrower communicate with the lender’s law firm rather than the lender directly.

Step 2: Notice of Sale Under Mortgage

The Notice of Sale can be sent2 once the property has been in default for at least 15 days. Once the Notice of Sale has been sent, the lender must wait at least 35 days (or 40 days if the property is occupied by a married couple3) before taking any further legal action. The 35 to 40 day waiting period gives the homeowner time to prevent the mortgage default or arrange another mortgage.

If you are unaware of any mortgage default, we recommend that you contact the lender to clarify the default. The Notice of Sale will confirm that your property is now in Power of Sale and give instructions on resolving the matter.

A sample of a Notice of Sale is below. The notice will state how much principal is owed and any other fees such administration, inspection and legal fees.

Step 3: Redemption Period

In every Notice of Sale document, there should be a breakdown of the costs owed to the lender and a payment deadline. The time between the notice being sent and the deadline is known as the “Redemption Period4.” During this period, if the borrower is able to pay all missing payments plus fees, the borrower may resume the mortgage as usual. This is commonly referred to as “putting the mortgage back in good standing.” It is usually preferable to pay the outstanding mortgage balance amount than to proceed to the next stages of the legal process. Many homeowners sell their possessions or take personal loans for this purpose.

If the borrower fails to make payment before the deadline, the lender can request the return of the entire mortgage balance, which includes the principal money. Some mortgages, such as expired mortgages or Home Equity Lines of Credit (HELOC), may not provide a Notice of Sale or Redemption period. In these cases, the lender may request full repayment immediately instead of simply repaying missing payments plus fees.

Step 4: Statement of Claim or Possession Steps

Once the Redemption Period for the Notice of Sale has expired, the lender can send the Statement of Claim5. A Statement of Claim for a mortgage can be a Power of Sale or a Foreclosure in Ontario. The legal process used will be made clear in the title of the document. The Statement of Claim is filed with the court and sent to the homeowner. The claim will have a court file number and a filing date, along with the amounts owed.

In Ontario, Power of Sale is the most commonly used legal process since it is generally faster and incurs fewer fees than Foreclosure. In most mortgage contracts in Ontario, there is a clause that states that all fees incurred while administering the mortgage are charged back to the mortgage. This means that the legal bills incurred while under Power of Sale are charged back to the mortgage. Since these fees can exceed $30,000, homeowners should act quickly to halt the Power of Sale proceedings.

Notice of Possession and Writ of Possession

It is important to understand the difference between a Notice of Possession and Writ of Possession. The Notice of Possession can be sent once the lender has received judgment6 on the Statement of Claim. The notice will be sent to the court requesting that the lender be given possession of the property. The court then must agree to give possession to the lender.

Many homeowners think that once they receive the Notice of Possession they must vacate their home. This is not correct. The Notice of Possession does not mean that the homeowner must vacate the property by a certain date. The Notice of Possession is sent to the court to request a Writ of Possession7. If a Writ of Possession is granted, the lender will have the court’s permission to evict the occupants of the property. A copy of the Notice of Possession is also sent to the property owner.

A Writ of Possession is sent to the sheriff to set an eviction date8. Avoiding an eviction at this stage in the legal process can be very difficult. Usually, the lender will only accept a total repayment of their mortgage.

Filing a Statement of Defence for a Mortgage

Many people feel that the lender has misused the Power of Sale process to take advantage of them. The Statement of Claim informs every person that they have the right to file a Statement of Defence9 in response to a Statement of Claim.

For a mortgage related statement of defence the defendant must provide reasons as to why the statement of claim is not correct. For instance, if the address of the property or name of the owner is wrong then this could be a defence that a judge might agree with and discharge the claim.

Stating that the borrower could not make the monthly mortgage payments because they were out of the country or laid off from work is not considered to be a good reason to discharge the claim. Saying that you did not receive the legal documents and, therefore the claim is not valid.

Filing a statement of defence can be an expensive and time-consuming process. The borrower may gain an additional few weeks of time, but it could cost thousands of dollars. In many cases, a mortgage-related defence is not accepted by the judge, and there is no benefit to the borrower.

Notice to Vacate or Eviction Notice

If you have received a Notice to Vacate or Eviction Notice, you must act quickly to save your home. A notice to vacate usually means that the local sheriff will evict all occupants from the property within a week or two.

You can call the local sheriff’s office to confirm that the Notice to Vacate is valid. The contact information should be on the notice to vacate. The sheriff’s office can confirm that the eviction notice is valid and can confirm the date and time of the eviction.

Every municipality has a different sheriff, so a sheriff in Toronto may have a different eviction schedule when compared to a sheriff in Hamilton or Oshawa. This is why it is important to call the sheriff’s office to confirm the eviction date.

If you are evicted, you still own the house, but your right to enter the house is limited. We advise that the owner remove all contents from the house before being evicted. If you are evicted, the owner can only enter the house with the permission of the mortgage holder. Usually, the mortgage holder requires that a property manager be present at the house to ensure that there is no damage. As the owner of the house, you still have the right to sell the house, but this can be difficult since the owner will not be able to show the house to potential buyers.

What Are Your Rights During Power of Sale?

If you need help to avoid or stop a Power of Sale our team can assist you. To understand your options we start by reviewing all the relevant information related to your situation. This includes determining how much is owed, value of the property and reviewing all legal documents.

In the majority of cases, the best way to prevent or stop a Power of Sale involves paying the lender the money they are demanding. The lender should provide a discharge statement which shows the amounts owed. This statement should show line items such as principal amount, mortgage arrears, penalties, legal fees, etc. We advise that the homeowner get a second opinion on the discharge statement just to confirm that the fees are justified.

If you don’t have the money on hand, you can seek out a private mortgage lender for financing. Most banks and other traditional lenders cannot approve a loan for a person in Power of Sale. Many private lenders specialize in high-risk lending and can overlook legal issues or issues with income and credit score.

Taking Immediate Action to Resolve the Issue

Due to the urgent nature of the situation, it is best for homeowners to take action immediately upon learning of the mortgage default.

1. Contact your mortgage lender – Most mortgage lenders want to help and work with their customers. They are primarily interested in the return on who their investments and may be willing to devise creative solutions with borrowers. Lenders typically do not want to go through the hassle involved with legally evicting homeowners. A lender may be willing to offer a payment plan or deferred payments to help homeowners get back on their feet.

2. Ask friends and family for help – If you have friends or family with money or property, they may be able to help. Borrowers from people you know will generally be cheaper than working with third-party companies. If the borrower is still in the Redemption Period, it may be easy to request the amount needed for good standing. If the entire mortgage debt is due, you may need to leverage the properties of friends and family to apply for a new mortgage.

3. Take out a private mortgage loan – In Ontario, there is a broad network of well-established and experienced private lenders who can negotiate private mortgage loan options despite any credit problems. Rates will generally be between 8% and 12%, and fees associated with these private loans tend to be between 3% and 6% of the total loan amount. Any loan that will be negotiated will not exceed 75% Loan-to-Value ratio (LTV) or 75% of the assessed value of your home.

The LTV ratio is the percentage of the property’s value owed in mortgages. If a homeowner has a home worth $1,000,000 with a $500,000 first mortgage and is requesting a $250,000 second mortgage, the LTV ratio for the requested mortgage can be up to 75% of the property’s value. All existing mortgages, plus all proposed mortgages, are divided by the appraisal value.

4. Sell your property As-Is quickly – If you cannot be approved for alternative financing, selling your home before the lender takes it may be your best alternative. Before selling, consider the following: Can you sell for a price that is able to pay off all debts? Do you have enough time to sell the house? If you can manage to get a firm purchase offer that pays off all mortgage debt, you may be able to stop the Power of Sale proceedings.

It is strongly recommended to get a real estate agent who court’s understands the Power of Sale process to assist with the sale. While these agents charge real estate commissions for their services, it is usually worth it since they can help you get a reasonable selling price and avoid legal issues. A good agent will be able to sell the property in its current condition, and ensure that all debts and closing costs are paid at the end.

5. Seek advice from mortgage professionals – Often, homeowners are overwhelmed and confused by the various jargon and different options available. While the methods previously mentioned work in most cases, it can be difficult to implement a solution on your own. Professionals like those on our team can easily break down your situation and explain your best options. Getting a free consultation at the minimum is strongly recommended. You can contact us for a free consultation at 416-499-2122 or by email at jonathan@powerofsalesontario.ca.

What to Do in the Next 24–48 Hours

- Do not ignore the lender’s notice.

- Find out exactly how much is owed.

- Gather your mortgage statement, Notice of Sale, property tax bill, income documents, and ID.

- Speak with a mortgage broker about refinance or private mortgage options.

- Contact a lawyer if legal enforcement has already started.

- Avoid waiting until the property is listed or sold.

Working with Private Mortgage Lenders

A mortgage from a private lender can be used to pay off the lender who is threatening the Power of Sale and stop the legal process. Once the new mortgage is set up, the private lender can negotiate with the existing lenders and pay them directly to stop any legal actions. Most private lenders can approve a mortgage if the Loan-to-Value (LTV) ratio does not exceed 75%.

Advantages of Using a Mortgage Broker

Stopping a Power of Sale situation by yourself can be overwhelming, and you may find the services of a specialized mortgage broker to be helpful. A mortgage broker who is familiar with the Power of Sale process can quickly lay out your options and identify the best lenders for your situation. Our team at Mortgage Broker Store has over a decade of experience in stopping Power of Sales and foreclosures and preventing evictions. The first thing we do is take the time to listen to your situation, understand which stage in the Power of Sale process you are in, and give you a timeline and possible solutions. We can tell you quickly if you can get approved for financing or if you are better off selling the property. For free advice, call our team at 416-499-2122 or email jonathan@powerofsalesontario.ca.

About Private Lenders

Private lenders are widely available to help Ontario-based homeowners when it comes to the complexities of the Power of Sale process. At Mortgage Broker Store, we have access to a wide range of well-established and experienced private lenders across the province that will be able to negotiate various private mortgage loan options, from debt consolidation loans to Home Equity loans and Lines of Credit.

Private mortgage loans will help you settle mortgage arrears on your existing mortgage and ensure future payments are manageable. Don’t hesitate to contact us at your convenience to help us discuss your options when it comes to stopping any Power of Sale on your valued and cherished home.

Need Power of Sale advice? Speak with us, and we’ll connect you directly with a Power of Sale lawyer you need. We have you covered. Call 416-499-2122 or email jonathan@powerofsalesontario.ca and gain expert advice! Please note that we are not lawyers and do not provide legal advice.

References

- Rules of Civil Procedure, R.R.O. 1990, Reg. 194, Rule 14 and Rule 64 — commencing a Statement of Claim and mortgage actions ↩︎

- Mortgages Act, R.S.O. 1990, c. M.40, ss. 31–33 — Notice of Sale timeline, form, and service ↩︎

- Family Law Act, R.S.O. 1990, c. F.3, ss. 21–22 — matrimonial home rights of married spouses ↩︎

- Mortgages Act, R.S.O. 1990, c. M.40, ss. 42–43 — proceedings during the notice period and redemption rights ↩︎

- Rules of Civil Procedure, R.R.O. 1990, Reg. 194, Rule 14 and Rule 64 — commencing a Statement of Claim and mortgage actions ↩︎

- Rules of Civil Procedure, R.R.O. 1990, Reg. 194, Rule 19 — default proceedings ↩︎

- Rules of Civil Procedure, R.R.O. 1990, Reg. 194, Rule 60.03 and Rule 60.10 — enforcement of possession orders and the Writ of Possession ↩︎

- Rules of Civil Procedure, R.R.O. 1990, Reg. 194, Rule 60.03 and Rule 60.10 — enforcement of possession orders and the Writ of Possession ↩︎

- Rules of Civil Procedure, R.R.O. 1990, Reg. 194, Rule 18.01 — deadline for delivering a Statement of Defence ↩︎

Disclaimer

Information regarding power of sale, foreclosure, and related legal processes is provided for educational purposes only and should not be relied upon as legal advice. Laws and procedures may change. Readers should consult a qualified lawyer regarding their specific situation.

Frequently Asked Questions (FAQ)

Get clear answers on stopping a power of sale in Ontario.

These common questions explain what to do after a Notice of Sale, how private mortgage options may help, and why acting quickly can protect more of your options.

How quickly can you help me stop a power of sale in Ontario?

We can review your situation quickly, confirm what stage you are in, and explain whether refinancing, a private mortgage, selling, or negotiation is the best option.

Can I stop a power of sale after receiving a Notice of Sale?

Yes, a power of sale can often be stopped after a Notice of Sale if you act quickly, pay the arrears, arrange financing, refinance, sell, or negotiate with the lender.

What does it cost to stop a power of sale with a private mortgage?

Private mortgage rates are generally 8% to 12%, with fees often between 3% and 6% of the loan amount, depending on equity and risk.

Can I stop a power of sale if I have bad credit?

Yes, private lenders may still consider you because they can often overlook credit problems and focus more on your property equity.

Can I stop a power of sale if I am self-employed?

Yes, private lenders may consider non-standard income, including freelance or contract income, when traditional lenders may not.

How does a second mortgage help stop power of sale?

A second mortgage can provide funds to pay the existing lender, settle arrears, and stop the legal process before the property is sold.

What documents do I need to stop a power of sale?

You should gather your mortgage statement, Notice of Sale, property tax bill, income documents, ID, and any other documents related to the power of sale.

Can I sell my house before the lender sells it?

Yes, homeowners can sell before the lender sells the property, and a firm offer that pays off the mortgage debt may stop the power of sale.

What areas of Ontario do you help with power of sale?

Power of Sales Ontario helps Ontario-based homeowners and has access to private mortgage options across the province.

Is it too late to stop power of sale if my home is already listed?

Not always, but your options become more limited once the property is listed, so you should act immediately before the property is sold.

Areas We Serve

We help homeowners stop power of sale and foreclosure across Ontario. Get local power of sale support in your city:

- Stop Power of Sale in Toronto

- Stop Power of Sale in Hamilton

- Stop Power of Sale in Brampton

- Stop Power of Sale in Burlington

- Stop Power of Sale in Oshawa

- Stop Power of Sale in Barrie

- Stop Power of Sale in Waterloo

- Stop Power of Sale in Niagara Falls

- Stop Power of Sale in Caledon

- Stop Power of Sale in Stouffville

View all cities we serve in Ontario or find your local Court Enforcement Office.

Google Reviews

What Our Clients Say

4.8 Based on 72 Google reviews

I had a quick call with Jonathan and was genuinely impressed by how knowledgeable, patient, and helpful he was. He took the time to listen to my situation and offered clear, tailored advice that made me feel more confident and informed about my next steps. It’s not easy to find someone who combines expertise with… Read more on Google

I found the website on google, looking for some information regarding a legal matter that I’ve never been involved with. Fortunately a quick conversation with Jonathan Alphonso put my mind at ease with all the questions and guidance that I needed to move forward. Thank you again Jonathan. I will continue to visit your website… Read more on Google

I reached out to Power of Sales Ontario and had pleasure of speaking with Jonathan Alphonso. His willingness to help me in a time where I didn’t understand or even where to begin was truly impressive. He answered my numerous questions over several encounters, providing me with extensive information; giving me a better perspective of… Read more on Google