A power of sale in Ontario is the legal process that lets a mortgage lender sell a property after the borrower defaults, without going to court to take ownership. The homeowner remains the owner until the sale closes and can stop the process by paying the arrears or the full mortgage debt before key deadlines.

The Power of Sale Process

A Power of Sale is the most common mortgage remedy used by mortgagees of land in Ontario. When a borrower fails to uphold the terms of the mortgage, a Power of Sale can be used to recover the lender’s principal, interest and expenses. The lender must follow a strict process in order to follow through with the eviction of the mortgagor and the eventual sale of the property. This process is different from the commonly known, but less used in Ontario, foreclosure. There are many notices and deadlines before and during this process that homeowners should be aware of. The individual timelines may vary according to the specific mortgage agreements and contracts signed.

What Is A Power of Sale in Ontario?

In a power of sale, the lender, known legally as the mortgagee, uses its rights under the mortgage to sell the property after the homeowner defaults. The homeowner, called the mortgagor, remains the property owner until the sale is completed but may have an opportunity to correct the default before certain deadlines pass. The lender then applies the sale proceeds toward the mortgage debt, legal costs and other valid claims, with any remaining funds paid to the person entitled to them.

| Topic |

Power of Sale

More Common

|

Foreclosure

Less Common

|

|---|---|---|

| General process | Lender sells the property | Lender seeks ownership through court |

| Who retains ownership before completion | Homeowner | Homeowner until court process changes title |

| Treatment of surplus | Generally distributed after debts and costs | Different consequences after foreclosure |

| Possible shortfall | May remain recoverable | Legal consequences differ |

| Use in Ontario | More commonly used | Less commonly used |

The Power of Sale Timeline in Ontario

Step 1: The Borrower Defaults on the Mortgage

The Power of Sale process begins after the borrower breaks the terms of the mortgage agreement. Typically, the borrower has failed to make one or more mortgage payments. Other defaults include the breach of a covenant in the mortgage: failure to insure the property, pay realty taxes, purposefully damage the property, or use the property for illegal use or activity. In the case of a breach of covenant, the lender must contact the borrower in writing to notify them that they are defaulting on the mortgage terms and give them an opportunity to remedy the default. Failure to make mortgage payments is not a requirement.

Step 2: The Lender Delivers a Notice of Sale and Related Notices

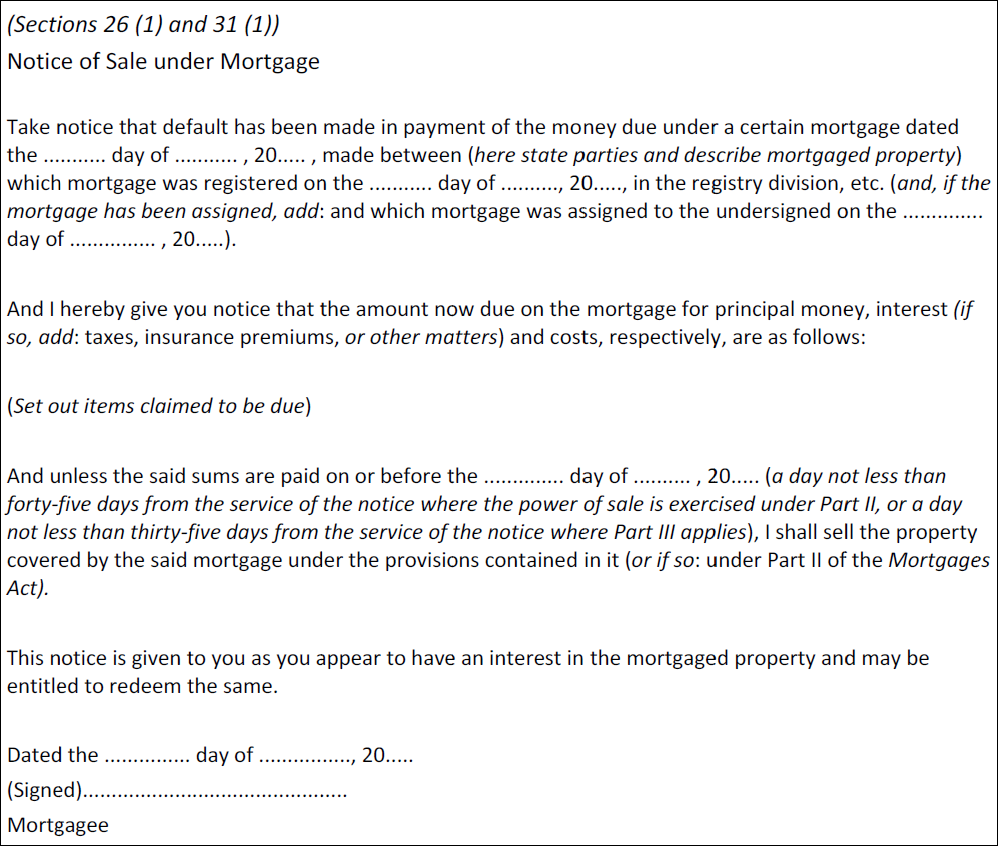

Under section 32 of Ontario’s Mortgages Act1, a Notice of Sale Under Mortgage cannot be delivered until the default has continued for at least 15 days. There is also a requirement to give notice under the Bankruptcy and Insolvency Act2 and the Farm Debt Mediation Act, the latter two notices being mailed to the mortgagor in advance of delivery of the Notice of Sale.

The form, contents and required recipients of the Notice of Sale are set out in section 31 of the Mortgages Act3 and the prescribed Form 1 under O. Reg. 814/214. Under section 33, the notice is given by personal service or by prepaid registered mail to every party shown as a mortgagor or guarantor, as well as all other parties with an interest in the mortgaged property, including subsequent mortgagees, lien holders and execution creditors.

After the Notice of Sale is given, section 32 of the Mortgages Act prohibits the sale for at least 35 days, and section 42 bars the lender from taking further proceedings during the notice period without a court order. Where the property is a matrimonial home, section 22 of Ontario’s Family Law Act5 entitles the spouse to the same notice and right of redemption, which in practice extends the waiting period to 40 days when the notice is mailed.

Step 3: The Borrower is Given Time to Pay Off the Mortgage Debt

The waiting period after the Notice of Sale is delivered is referred to as the redemption period. This right is protected by sections 22 and 43 of the Mortgages Act6: a borrower who pays the arrears (or the full amount demanded) plus the lender’s enforcement costs within the notice period is relieved from the consequences of the default, and the lender is bound to accept payment made in accordance with the notice. During this time, the borrower must either bring the mortgage into good standing if it is not due or pay off the entire mortgage debt, including legal fees incurred by the lender to enforce their rights.

If the mortgagor does not pay what is owed prior to the expiry of the redemption period, the lender is able to issue a Statement of Claim for the collection of the debt owed and for possession of the property. With the eviction of the mortgagor and others living at the property, the lender can follow the approved practices, which will allow them to list the property for sale on MLS.

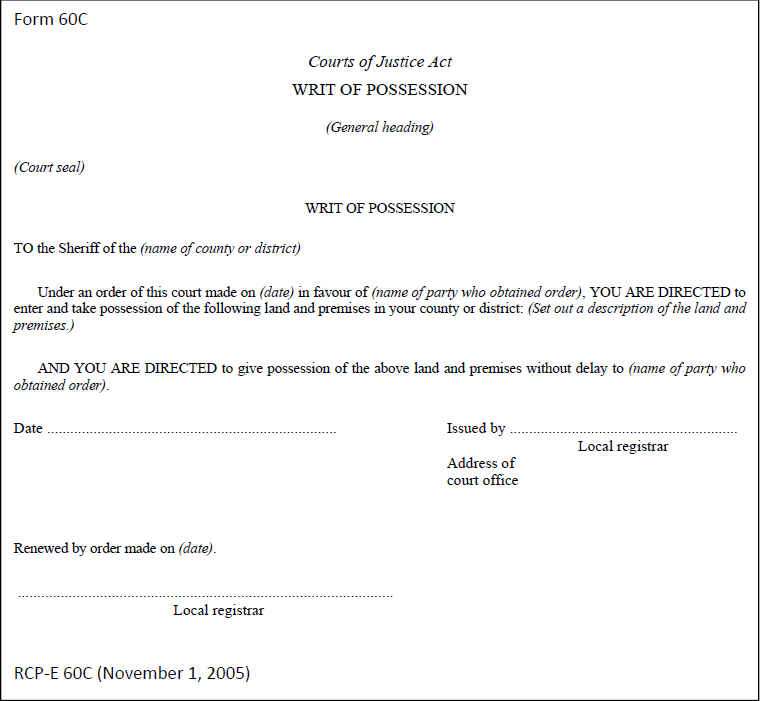

Step 4: The Lender Applies to Take Possession of the Property

After the Statement of Claim is issued and served, if the mortgagor does not file a Statement of Defence, the lender can sign a default judgment. After signing a default judgment, the lender must bring a court motion to ask the court for leave to allow for the issuance of a Writ of Possession7. Once the Writ of Possession is issued by the court office, the lender delivers it to the sheriff of the jurisdiction in which the mortgaged property is located. The sheriff schedules a date to evict the mortgagors (often the homeowner and their family) and gives them an opportunity to move out of the house. If they do not move out voluntarily, the sheriff will attend and arrange for the removal of the occupants.

Step 5: The Lender Evicts the Homeowners and Takes Possession of the Property

Once the homeowners are evicted, the lender will proceed to sell the home, typically using a licensed real estate agent. To protect the lender, two appraisals of the property are secured as the lender must ensure that he sells the property for market value. Special clauses are inserted into the offer that clearly states that the property is being sold on an “as is” basis.

Step 6: The Property is Sold, and the Proceeds From the Sale Are Used to Pay Off Debts

When the sale is completed and the money is received, the proceeds of the sale are paid out in the following order:

- The expenses incurred by the lender in selling the property are paid first. This includes the real estate agent’s fee, the real estate lawyer’s fees, and other related fees and expenses.

- Payment of the lender’s principal and interest and other sums to which the lender is entitled are next to be paid from the proceeds of the sale.

- If any funds are left over after the previous payments then payment is made to subsequent mortgagees, lien claimants and execution creditors in the priority in which they were registered until the funds are exhausted.

- Any remaining money after all other parties have been paid must go to the former homeowner.

Often, the costs associated with conducting the Power of Sale process are such that the homeowner will receive little to no proceeds from the sale of the property. In addition, if the mortgage lender is unable to fully recover their entire investment principal, they can file a Writ of Execution for the remaining sum owed with the local sheriff.

Important Legal Notice

Always remember that the above discussion about the Power of Sale process is for informational purposes only and is not an exhaustive discussion of the entire process available to a mortgage lender in the face of a mortgagor’s default. Any lender who is experiencing a mortgage default should seek legal advice as to how they should proceed. In addition, the borrower has rights in the face of a Power of Sale and should consult a lawyer when they receive a Notice of Sale Under Mortgage.

References

- Mortgages Act, R.S.O. 1990, c. M.40 — Parts II and III (statutory powers and notice of exercising power of sale) ↩︎

- Bankruptcy and Insolvency Act (Canada), s. 244 — notice of intention to enforce security ↩︎

- Mortgages Act, R.S.O. 1990, c. M.40 — Parts II and III (statutory powers and notice of exercising power of sale) ↩︎

- O. Reg. 814/21: Forms — prescribed Form 1, Notice of Sale Under Mortgage ↩︎

- Family Law Act, R.S.O. 1990, c. F.3, ss. 21–22 — matrimonial home consent, notice and redemption rights ↩︎

- Mortgages Act, R.S.O. 1990, c. M.40 — Parts II and III (statutory powers and notice of exercising power of sale) ↩︎

- Rules of Civil Procedure, R.R.O. 1990, Reg. 194 — court possession procedures ↩︎

Frequently Asked Questions (FAQ)

Get clear answers about the power of sale process in Ontario.

These common questions explain how long the process takes, how it can be stopped, and what the key notices and documents mean.

How long does a power of sale take in Ontario?

The Notice of Sale cannot be delivered until the default has continued for at least 15 days, and the lender is then barred from selling for at least another 35 days (40 days when the notice is mailed for a matrimonial home). If the debt is not paid, the court steps that follow — Statement of Claim, Writ of Possession and eviction — mean the full process usually takes several months from the first missed payment to a completed sale.

Can I stop a power of sale after it starts?

Yes. Under the Mortgages Act, a borrower who pays the arrears or the full amount demanded, plus the lender’s enforcement costs, within the redemption period is relieved from the default, and the lender must accept that payment. See our guide on how to stop a power of sale in Ontario for all of your options.

What does “sold under power of sale” mean?

It means the mortgage lender, not the homeowner, is selling the property after a mortgage default. The home is typically listed with a licensed real estate agent and sold on an “as is” basis, and any money left after the mortgage debt, selling costs and other registered claims are paid belongs to the former homeowner.

What must a Notice of Sale contain?

The form and contents are prescribed by section 31 of the Mortgages Act and Form 1 under O. Reg. 814/21. It sets out the amounts owing and the deadline to pay, and it must be served personally or by registered mail on every mortgagor and guarantor, plus anyone else with an interest in the property. Read more in our Notice of Sale guide.

Need Power of Sale advice?

Speak with us, and we’ll connect you directly with a Power of Sale lawyer you need. We’ve got you covered. Call 416-499-2122 or email jonathan@powerofsalesontario.ca and gain expert advice!

Discover more about deed in lieu of foreclosure by clicking deed in lieu of foreclosure And more about strict foreclosure strict foreclosure

Disclaimer: This page is for general informational purposes only and should not be taken as legal, financial, mortgage, or real estate advice. Power of sale and foreclosure matters can have serious consequences, and you should speak with a licensed mortgage professional, lawyer, or qualified advisor before making decisions. Power of Sales Ontario does not guarantee results, mortgage approval, or that the information on this page applies to your specific situation.