Managing a mortgage can seem like an impossible challenge in Ontario. When interest rates rapidly fluctuate while prices remain high, it can be hard to bounce back when your mortgage payments stagnate. However, homeowners have time to intervene and correct the problem before it snowballs. If you are honest with your lender about your financial status and pathways to take, you can avoid losing your home. This article discusses everything you need to know if you struggle to afford your mortgage.

Signs You’re Struggling with Mortgage Payments

Money troubles often grow slowly, getting serious before you fully see them. Noticing early signs lets you act before things get worse. One flag that you’re struggling to keep up with your mortgage payments is if you are paying them late more frequently than on time. Another telltale sign is if you’re using credit cards or loans to cover everyday costs. Weighing which bill to pay first, like utilities, loans, or your mortgage, is another sign.

Using your savings or emergency fund to make mortgage payments is another negative sign. It’s okay to spend your savings occasionally, but you should never make a habit of it. If you’re forced to skip essentials like food or medical care to make mortgage payments, that’s a red flag. Quick action can prevent things from spiralling out of control.

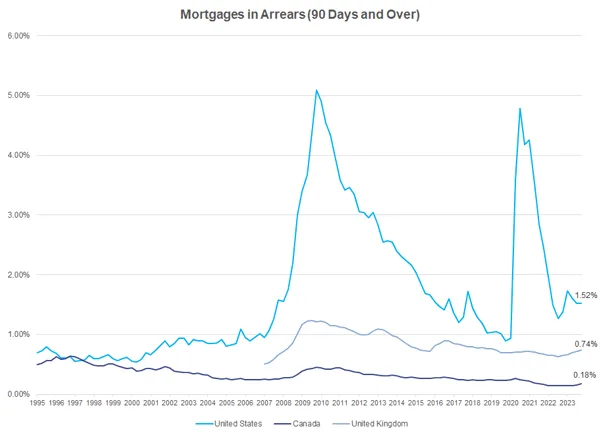

Mortgages in Arrears

“Mortgages in arrears” refers to mortgage payments that have not been made by the due date, resulting in the borrower being behind or overdue on their scheduled payments. Typically when payments are missed or delayed. The arrears amount is the total of missed payments plus any interest, penalties, or fees associated with late payments.

Source: https://cba.ca/article/mortgages-in-arrears

When mortgages fall into arrears, lenders may initiate steps toward foreclosure or power of sale proceedings if the borrower cannot resolve the overdue balance.

Talking to Your Lender

When you can’t keep up with your mortgage, immediately call your lender. Lenders like it when homeowners sneak up early instead of missing payments without a word. Seizing homes and repossessing property costs them money and time, so it is used only as a last resort.

Be clear to your lender about your financial challenges, like losing a job, enduring a family change, or facing surprise expenses. Many lenders can provide temporary relief, like letting you skip a few payments, paying only interest for a while, or changing how the loan works. Reaching out early might also save your credit score, as some lenders won’t report late payments if you’re actively remedying the problem.

Government Assistance Programs – Ontario-specific relief options for struggling homeowners

Struggling to keep up with your mortgage? Ontario has options to ease the pressure. The Ontario Electricity Support Program (OESP) can lower your utility costs, freeing up funds for your home payments. Property tax relief programs may potentially help you decrease your tax bill. In certain regions, local governments enable homeowners in difficult situations to delay or cut property taxes temporarily, allowing you to prioritize your mortgage.

The Ontario and federal governments may offer specific assistance during economic downturns, like recessions or crises. These programs may allow you to halt mortgage payments, acquire lower interest rates, or obtain financial relief to prevent losing your house. Because these programs change with the economy, check regularly with provincial housing authorities or local offices to stay informed about available help.

Refinancing and Debt Consolidation

Looking to stretch your monthly budget? Mortgage refinance or debt consolidation might help. When you refinance, you exchange your current mortgage for a new one, typically locking in a lower interest rate or extending the payment period. It can cut your monthly costs, freeing up funds for other needs.

Debt consolidation is a different approach. It consolidates high-cost obligations, such as credit balances or personal loans, into a single, simpler loan. Many homeowners achieve this by leveraging their mortgage or opening a home equity line of credit. Consolidating your loans may help you reduce your monthly payments and make managing your mortgage easier.

Nonetheless, there are still numerous things to consider as paying off your existing loan early may result in expenses such as appraisal costs, legal fees, or fines. You also need enough equity in your home to make it work. A mortgage expert can guide you in deciding if these steps suit your financial situation.

Power of Sale

If you can’t catch up on missed mortgage payments after trying to talk to your lender or refinance, your lender in Ontario might start a Power of Sale. It allows them to sell your home to get back the money you owe on the mortgage. Unlike foreclosure, which takes a long time in court and has the lender take the home, Power of Sale is more efficient, with the lender having the right to sell the property without owning it first.

When a Power of Sale starts, you’ll get a Notice of Sale, giving you about 35 days to pay what you owe plus fees or make a payment plan (or 40 days if occupied by a married couple). You need to move fast to keep your home. Lenders sell the property at market value, and any money left after paying the mortgage and sale costs goes to you. But this can hurt your credit, so try to avoid it.

Seeking Professional Advice in Ontario

Managing mortgage payment concerns on your own may be intimidating. Mortgage brokers, financial planners, credit counsellors, and attorneys can all be beneficial resources. A mortgage broker can look into refinancing or find lenders who provide payment choices that are suitable for you.

Lawyers who know about real estate and mortgage laws can tell you your rights, talk to your lender for you, or help with a Power of Sale. Community financial counselling can also help by making budgets, cutting extra spending, and planning how to pay off debts. Getting advice early can reduce money problems and help you keep your homeownership status.

Facing Mortgage Affordability Issues Head-On

Struggling to pay your mortgage in Ontario is hard, but pretending it’s not happening worsens the situation. Recognizing financial problems early, calling your lender quickly, looking into government help, and thinking about refinancing or consolidation are important steps. Knowing your rights during a Power of Sale and getting expert advice when you need it can save your home.

Keeping your mortgage affordable takes effort and clear decisions. Your financial health depends on acting fast and smart. By staying informed, asking for help, and checking out your options carefully, you can power through these problems and keep your home even when times are tough. If you still have questions about mortgage affordability, please do not hesitate to contact us at jonathan@mortgagebrokerstore.com or 416-499-2122.

Disclaimer: This article is provided for educational purposes only and does not constitute mortgage, legal, tax, financial, or investment advice. Mortgage products and lending criteria vary by lender and borrower circumstances. Readers should seek professional advice before making financial decisions.