Tariffs and Mortgage Defaults: Are More Power of Sale Homes Coming?

Tariffs are driving up the cost of consumer goods and increasing inflation at the same time. This is putting pressure on homeowners and spiking the number of mortgage defaults. A big surge in the power of sale properties may be coming soon.

That would mean there’s a risk for homeowners and an opportunity for investors and buyers.

Understanding Tariffs: What They Are and How They Affect the Economy

Understanding how tariffs work and how they might affect the Canadian mortgage industry starts with a definition. Tariffs are taxes and duties a government imposes on exported and imported goods.

Consequences

Here are a few consequences. Industries that need to have a flow of raw materials or imported parts face higher production costs. Companies can reduce wages, close down shops, or lay off staff. They can also pass along those costs to consumers.

Exporting

Canadian businesses that rely on exporting goods to countries like the United States will see a drop in sales. Those businesses might be forced to look for other suppliers, which can drive the cost up. Major industries in Canada like manufacturing, automotive and agriculture can start shedding jobs.

In general, Canada can start looking like a riskier market as tariffs disrupt industry. That can mean reduced incomes and a loss of jobs, and more businesses can close.

Then, there are the specific consequences for people with a mortgage.

The Link Between Tariffs, Inflation, and Mortgage Payment Struggles

When tariffs are placed on imported goods, prices go up. Trump’s tariffs on steel and aluminum have raised manufacturing costs, which are passed on to consumers. In this situation, steel and aluminum items become more expensive.

That affects inflation because higher consumer prices drive inflation and the overall cost of living up

Prices will rise, meaning borrowers have less income. Canada’s retaliatory tariffs on US imports increase inflation because they drive up costs for consumers and manufacturers.

Missed Payments

If the cycle continues far enough, homeowners can default on a mortgage agreement when they miss mortgage payments. A borrower can also break the mortgage agreement by breaching a covenant, which can include damaging the property on purpose, using it for illegal activities, not paying the taxes, or insuring the property.

It’s important to remember that a lender must wait 15 days after default to deliver a Notice of Sale. This is a legal notification letting the borrower know the property can be sold if the mortgage debt is not cleared up,

How Higher Costs for Homeowners Can Lead to Mortgage Defaults

Here’s a scenario that shows how these higher costs can cause mortgage problems.

Given tariffs on imported and exported building materials like lumber, the cost of these materials can rise drastically. If a homeowner in Ontario is planning a repair or renovation, they can find higher costs than they anticipated.

Reduced Hours

Here’s another example: American tariffs can lead to a drop in demand in Ontario’s manufacturing sector, and workers can face reduced hours or be laid off.

In each of these scenarios, the worker might need to use savings to cover mortgage payments, and once that money is depleted, they can face a default.

There’s another temporary solution: a private second mortgage can provide a homeowner with the money to stop a power of sale or foreclosure. These are interest-only payments and usually last for one year. It’s important to keep in mind that they are a stop-gap measure that requires an exit strategy.

Are Certain Homeowners More at Risk? Key Demographics Affected

Some borrowers are at higher risk than others. The following groups would do well to look into a private loan as a backup strategy. Remember, these have a streamlined application process and bad credit applications are accepted.

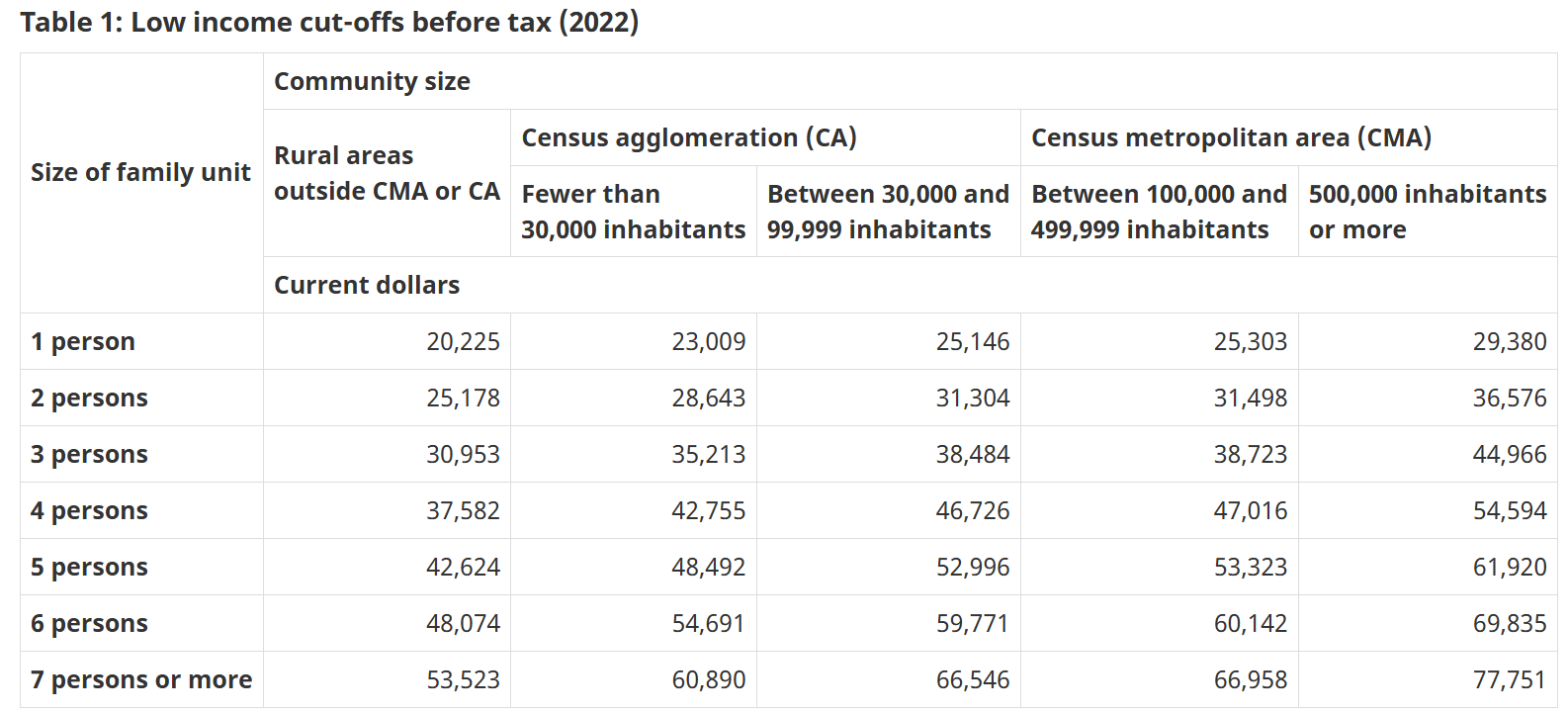

Low Income Earners

Homeowners who don’t have a lot of disposable income don’t have a very good financial cushion to absorb tariff-related costs. Here’s a table that highlights what constitutes the low-income cutoff point from the government of Canada.

Borrowers With Variable Rate Mortgages

A trade war involving tariffs can raise the cost of all goods and services, and the Bank of Canada can possibly raise interest rates to curb inflation. This can be a real issue for a variable-rate mortgage holder because their payments can go up.

These borrowers can already be struggling with rising prices in other areas and tariff-related expenses.

Borrowers in Specific Sectors

Of course, there are the homeowners who work in tariff-vulnerable industries like agriculture, manufacturing, and automotive. If a factory closes or stops production in any of these industries, housing prices can fall. Homeowners might not even be able to sell, and they could default on a mortgage.

Investment Opportunities: Is Now the Time to Buy Power of Sale Homes?

The last step of a power of sale process involves the lender evicting the homeowners and taking possession of the property. The next stage is where the property is sold. If you’re considering one of these homes as an investment opportunity, there are some good reasons to consider taking the plunge.

- The lenders are usually motivated to sell the property quickly. They’re usually looking to minimize any losses, which means an investor can quickly pick up a power of sale property for resale or renovation.

- Many of these properties need repairs and renovations so an investor can add value. They can boost their overall return by renting it out or improving the condition of the place to add value.

Even though tariffs are looming on the horizon, the 2025 TRREB Market Outlook and Year in Review Report predicts that there will be 76,000 home sales in Toronto this year, which would mean a boost of 12.4% over 2024. That’s for The GTA.

Of course, in the best case scenario, people who own homes will be able to keep them during the looming trade war. Here are a few tips that can help.

Tips for Homeowners: How to Avoid Default in an Uncertain Economy

Avoiding a power of sale means keeping your financial powder dry even during these difficult times. Here are a few boxes that you can check so you can keep your finances and mortgage payments up in spite of more impending tariffs.

Building Up An Emergency Fund

A big part of building an emergency fund is having the discipline to start. Putting a small, manageable amount away monthly or weekly is a good idea. Start with a small amount of $20, that can build up over time. Or you can decide to add to that as your finances change.

Either way, making consistent contributions will give you a buffer against defaulting on your mortgage.

Make Your Mortgage Payments The Priority

Ensuring you have the money to pay your mortgage on time can mean setting up automatic payments through your financial institution. Ensure the account you pick always has the funds in it because you’ll want to avoid overdraft charges.

It’s good to check with your institution to see if they have any offers. Some might offer fee-free paymentsor utilities and mortgages.

One other way to avoid defaulting on your mortgage is to look into a private second mortgage or loan. These are equity-based, and the payments are interest only. However, they’re an excellent solution if you need some money quickly to stop a power of sale or foreclosure while you fix your finances.

Got bad credit? It doesn’t matter when you’re looking for one of these private loans. Get in touch with us today to learn more about this opportunity that can act as a buffer against tariffs. Call 416-499-2122 or email ron@powerofsalesontario.ca.